It’s November, so you’re no doubt focused on the most important things of the season: getting snow tires on your car, making year-end holiday plans and … contributing to your bonus to your registered retirement savings plan (RRSP)?

If you’re already aware of the huge benefit that contributing to an RRSP can have on your finances and have made arrangements for your 2017 contribution, well done! You can now get back to planning your December getaway.

If you’re sitting there thinking that a new boat is a better use of your year-end bonus than socking away money in an RRSP, read on to see how you could be missing out on a major financial opportunity. You’ll thank yourself later for the foresight that a new fishing boat today could be a yacht in years to come with help from an RRSP.

The 60-second RRSP refresher

If you’re a bit fuzzy on what an RRSP is and how it works, here’s a quick reminder of why this powerful investment tool belongs in your financial plan.

The basic premise of an RRSP is straightforward: it’s about delaying the timing of when you pay income tax. This may not sound overly interesting or significant, but the impact on your finances can be huge.

Directing your bonus to your RRSP allows you to invest pre-tax income, separating it from your taxable income before the government takes a big bite out of it. As the investments within your RRSP account grow over the years, any dividends, interest and capital gains that they accumulate are not taxed. By starting with a larger pre-tax amount and avoiding tax deductions as it grows, your RRSP has the potential grow much larger compared to investments made over the same period that are not tax-protected.

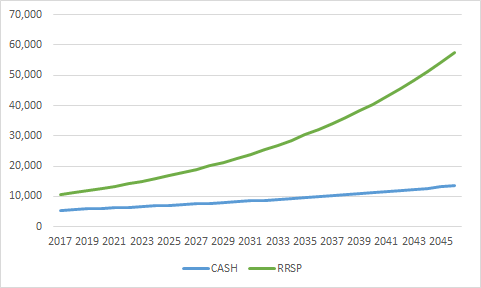

Reap the rewards of tax-protected investment

The graph below illustrates the difference between contributing a bonus of $10,000 towards your RRSP vs. getting your bonus in cash (taxed at 47%) and in both cases a growth of 5% p.a.

You will have to pay tax eventually – when you withdraw from your RRSP in the future, you will owe income tax on these withdrawals. However, by that time you will likely be retired with a significantly lower annual income compared to now, so most likely your income tax rates will also be lower.

Follow the rules or pay a price

To take advantage of the great benefits offered by RRSPs, you need to play by the rules. This means staying within the contribution limits. For the 2017 tax year, individuals are allowed to contribute up to 18% of their income or $26,010 – whichever is lower.

Some factors can reduce this amount (e.g. contributions made to your employer’s pension fund), while others can increase it (e.g. unused contribution room from a previous year). You can find your contribution room for 2017 on your latest notice of assessment from Canada Revenue Agency (CRA).

In general, withdrawing funds from your RRSP before you retire will result in a considerable penalty, so this is something to avoid unless absolutely or strategically necessary. There are exceptions when early withdrawals are allowed – such as to pay for education or buy a house – but these withdrawals must meet specific criteria. To ensure you don’t accidentally break the rules, it’s always a good idea to consult your financial advisor before withdrawing.

Don’t miss the deadline

Timing is also critical when it comes to your RRSP. To be counted by CRA as an RRSP contribution for the 2017 tax year, it must be made by 1 March 2018. If you miss this deadline, you’re out of luck.

While this is the official government deadline, your employer may set earlier deadlines to direct your bonus towards your RRSP to ensure they can process your request in time.

To ensure you don’t miss this opportunity to contribute to your RRSP and reduce your 2017 tax bill, we recommend finding out your contribution room and directing the appropriate amount to your RRSP.

Today’s opportunity, tomorrow’s windfall

If you’re a working professional with a high income, maxing out your RRSP contribution is almost always the right decision. There are other complementary strategies to consider as well and we would gladly talk to you about them.

But for now, if you can muster the discipline to max out your RRSP contribution now, you’ll be thanking yourself 10 times over when you see how big your nest egg has grown.

If you would like help optimizing your use of an RRSP within your overall financial plan, Rubach Wealth can help. Contact us today to discuss how acting now can give you so much more to be thankful for in the future.

")